Securing car finance can be a daunting process, but with the right knowledge and preparation, you can drive away with a deal that truly benefits you. Understanding the nuances of car financing is crucial for making informed decisions and avoiding potential pitfalls. This article will guide you through the essential steps to maximize your car finance deal, ensuring you get the best possible terms and a car that fits your budget. From researching lenders to negotiating interest rates, we’ll cover everything you need to know to become a savvy car finance consumer.

Understanding Your Car Finance Options

Before diving into the specifics, it’s important to understand the different types of car finance available. Each option has its own advantages and disadvantages, so carefully consider which one best suits your financial situation and needs.

- Hire Purchase (HP): You pay fixed monthly installments and own the car at the end of the agreement.

- Personal Contract Purchase (PCP): Lower monthly payments, but you don’t automatically own the car at the end. You have the option to buy it with a final “balloon” payment.

- Personal Loan: Borrow a lump sum from a bank or credit union and use it to buy the car outright.

- Leasing (Personal Contract Hire): You rent the car for a set period and then return it.

Key Factors to Consider

Several factors influence the overall cost and suitability of a car finance deal. Ignoring these can lead to paying more than necessary or ending up with a deal that doesn’t meet your needs.

- Interest Rate (APR): The annual percentage rate is the true cost of borrowing, including interest and fees. Shop around for the lowest APR.

- Deposit: A larger deposit typically results in lower monthly payments and a lower overall cost.

- Loan Term: A longer loan term means lower monthly payments, but you’ll pay more interest over the life of the loan.

- Credit Score: A good credit score increases your chances of getting approved for finance and securing a lower interest rate.

- Total Cost of Credit: Focus not only on monthly payments, but also on the total amount you’ll pay back, including interest and fees.

Negotiating Your Car Finance Deal

Don’t be afraid to negotiate! Dealers are often willing to lower the price of the car or offer a better interest rate to close a deal.

- Research the Car’s Value: Know the market value of the car you’re interested in before you start negotiating.

- Get Pre-Approved for Finance: Having pre-approved finance gives you leverage and shows the dealer you’re a serious buyer.

- Compare Offers: Get quotes from multiple lenders and dealers to compare terms.

- Be Prepared to Walk Away: If you’re not happy with the deal, be prepared to walk away. There are plenty of other cars and lenders out there.

The Importance of Credit Score

Your credit score plays a vital role in the car finance process. A higher score translates to better interest rates and loan terms. Take steps to improve your credit score before applying for car finance.

Improving Your Credit Score

- Pay Bills on Time: Late payments negatively impact your credit score.

- Keep Credit Utilization Low: Don’t max out your credit cards.

- Check Your Credit Report: Review your credit report for errors and dispute any inaccuracies.

- Avoid Opening Too Many Accounts: Opening multiple credit accounts in a short period can lower your score.

Comparison of Car Finance Options

| Finance Option | Advantages | Disadvantages |

|---|---|---|

| Hire Purchase (HP) | You own the car at the end of the term. Fixed monthly payments. | Higher monthly payments than PCP. |

| Personal Contract Purchase (PCP) | Lower monthly payments. Option to buy the car at the end. | You don’t automatically own the car. Mileage restrictions may apply. |

| Personal Loan | You own the car outright. No mileage restrictions. | May require a good credit score. |

| Leasing (PCH) | Lower monthly payments than HP or PCP. New car every few years. | You never own the car. Mileage restrictions apply. |

FAQ Section

What is APR?

APR stands for Annual Percentage Rate. It represents the total cost of borrowing money, expressed as an annual percentage. It includes the interest rate and any fees associated with the loan.

What is a balloon payment?

A balloon payment is a large, lump-sum payment due at the end of a PCP agreement. It’s the remaining value of the car that you need to pay if you want to own it.

Can I get car finance with bad credit?

Yes, it’s possible, but you’ll likely pay a higher interest rate. Consider improving your credit score before applying.

What is the best way to compare car finance deals?

Focus on the APR and the total cost of credit. Compare quotes from multiple lenders and dealers.

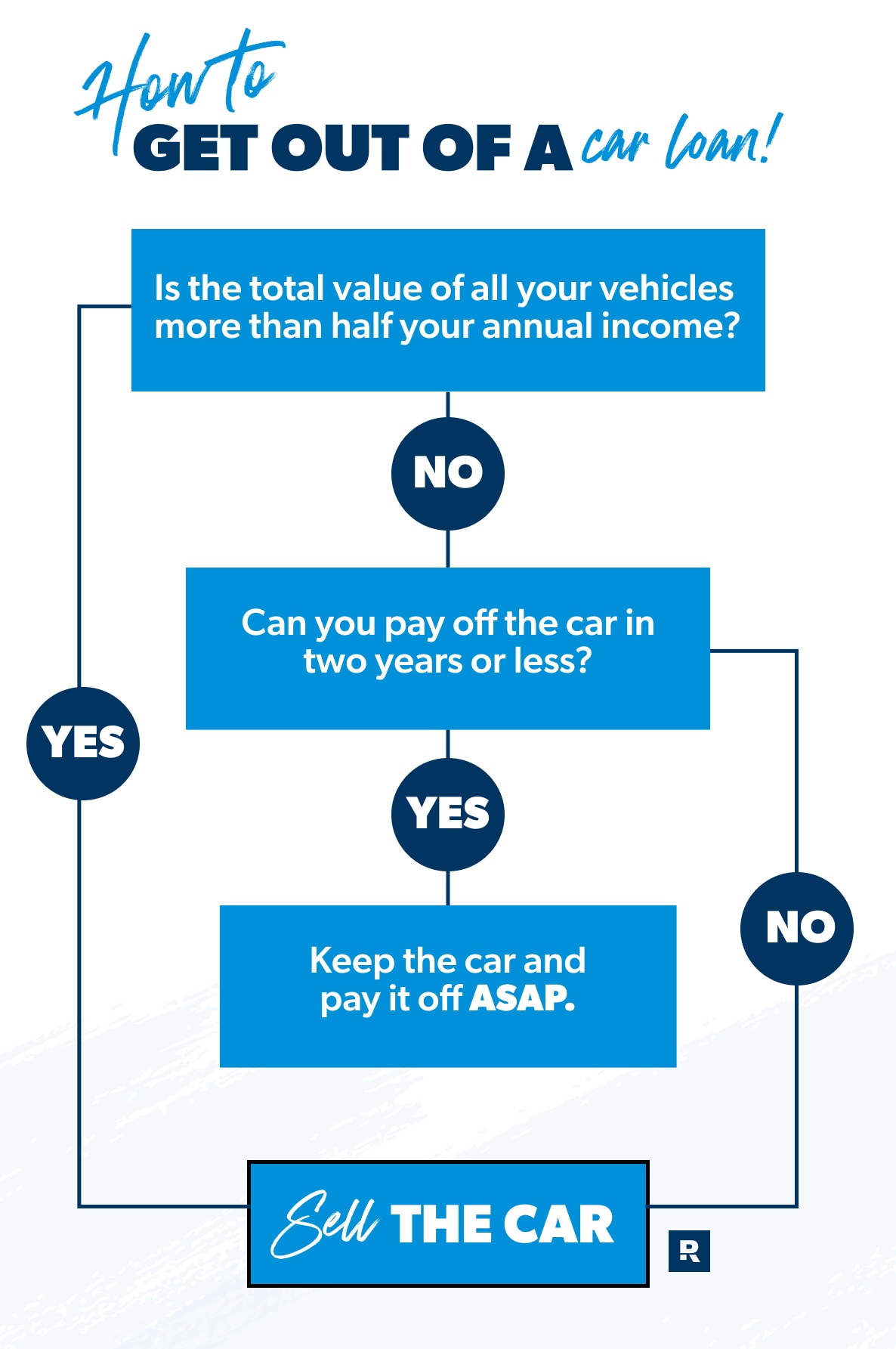

What should I do if I can’t afford my car payments?

Contact your lender as soon as possible. They may be able to offer a payment plan or other solutions.

Choosing the right car finance deal requires careful consideration and research. Don’t rush into a decision without fully understanding the terms and conditions. By comparing offers, negotiating effectively, and taking steps to improve your credit score, you can secure a car finance deal that works for you. Remember, the goal is not just to get a car, but to get a car under financial terms that you can comfortably manage over the loan period. Always read the fine print and ask questions if anything is unclear. With the right approach, you can drive away confident that you’ve made a smart financial decision.